China's Ticking Time Bomb

August 25, 2022

Russia’s terrible war against Ukraine dominates headlines and there’s little about the growing crisis in China. After three generations of sterling economic stewardship that’s created a middle class bigger than America’s population, China faces frightening fiscal and political headwinds. The country is owed $1 trillion by struggling governments around the world for Belt and Road Initiative projects, and its domestic real estate bubble is so gargantuan that much of its middle class has been damaged. A massive mortgage revolt is underway, banks are failing, and protests grow. Today, 100 million empty or unfinished units bought on “spec” in hundreds of urban areas may never be completed or paid for, enough to house half of all those who live in the European Union. This year, China’s debt is expected to reach the equivalent of 275 percent of its GDP due to massive borrowing and economic slowdown.

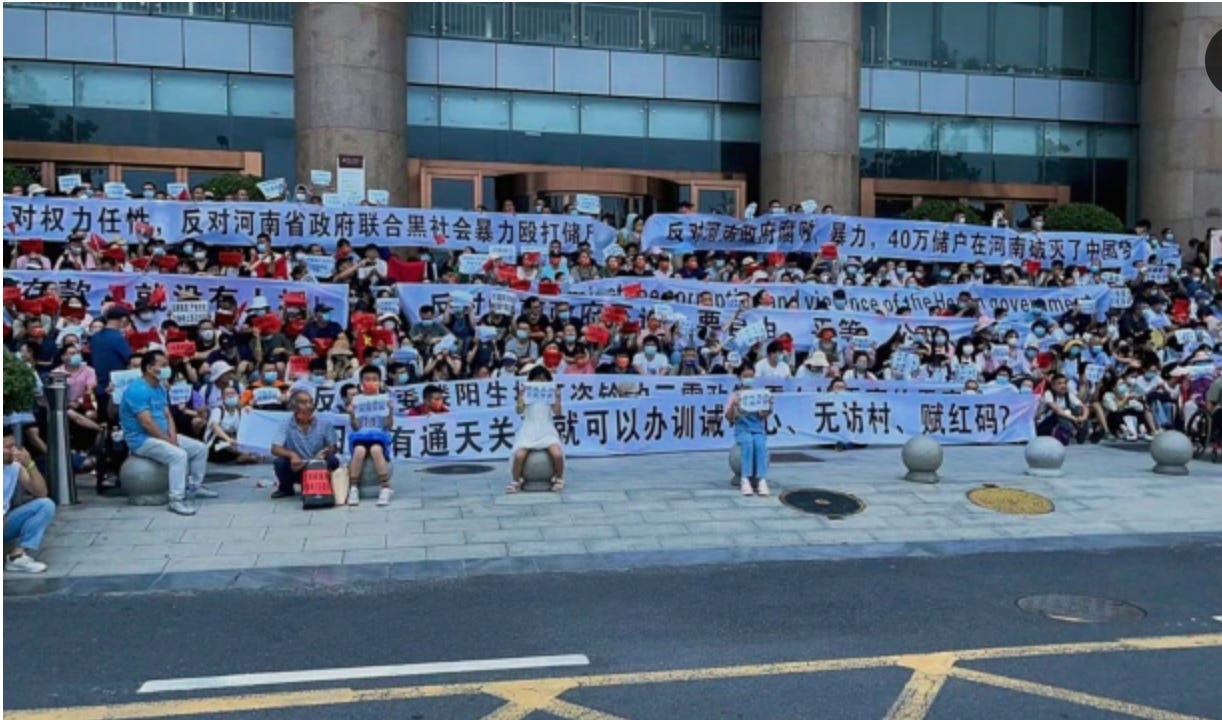

If you click on this footage here, you will see a rare glimpse of police violence against peaceful protesters that is starting to occur across the country. Unrest grows because real estate speculation has been widespread for years, and the Chinese consider property ownership as a way to get ahead and secure an adequate retirement income. But years of speculation has led to ever-increasing prices and overbuilding by aggressive developers and now there is a glut, collapse in prices, and widespread social discontent. Beijing is blamed, along with local governments, and all mentions of these troubles have been censored by the media and online. But unrest spreads by word of mouth which is a dangerous development in a country of 1.4 billion people where putting deposits and owning several condos had become commonplace.

Essentially, China is a debt disaster, in terms of foreign and domestic borrowing. At the same time, a cloud hangs over President Xi Jinping because of his diplomatic (albeit not military) support for Vladimir Putin’s genocide in Ukraine and energy attacks against Europe. These calamities converge as Xi faces re-election by the Politburo in November and has even led to grumbling that the country under his leadership may have reached the end of its peak influence and reputation. It’s not impossible that, if this unfolding political crisis in the streets grows, China’s Presidency may change or, worse, the Middle Kingdom may become unstable.

In rare acts of defiance, Chinese gather in public to object to the situation and millions are refusing to repay loans on their unfinished apartments. This massive mortgage boycott movement began in early July and has now spread to 100 cities involving 320 massive property development projects and many banks. Recently, China’s Politburo had to issue a statement assuring property buyers that the government would help cash-starved developers finish such projects and $44 billion will be dispensed to prop up their companies and their banks. But this is a paltry amount and millions of Chinese buyers need financial relief or else they will be left in the lurch.

“China's real estate slump has sucked in both banks and provincial governments, threatening a bigger impact on the world's second-largest economy,” wrote Nikkei Asia, an authoritative Japanese website. “Defaults have soared over the past 12 months. Real estate has been a key driver of the Chinese economy in the last two decades. Real estate and related activities now account for around 29 percent of gross domestic product, up from less than 10 percent at the end of the 1990s.”

The first crack appeared when Evergrande Group stopped paying its debts or finishing projects. It had obtained free land from politicians in smaller urban centers and mortgage financing from local banks, then convinced people to snap up multiple units in the belief that demand and prices would never drop.

Now China must bail out lower levels of government because they depended on revenue from these land sales in order to provide education, healthcare, retirement benefits and other social services to their communities. Their hardship means that services will be chopped, which could turn investor calamity into widespread national unrest. Clearly, China’s living standards have already suffered, given that one-quarter of its economy and more than 70 percent of its wealth has been tied up in real estate that has dropped in value.

A Wall Street Journal opinion piece headlined “Xi Tries to Ride a Real-Estate Tiger, and We All May Get Mauled” points out that these problems. The property bubble is bad enough but the country has also been economically damaged by Xi’s continuing pandemic lockdowns, his crackdown on tech entrepreneurs and on “corruption”. The Journal rightly concludes that this “places the entire Chinese economic miracle model at risk” and cautions that “global financial markets, central banks and democratic leaders should brace for turbulence”.

Then there is the Belt and Road Initiative debacle. Bloomberg reported that 19 emerging economies – such as Sri Lanka, Lebanon, El Salvador and Pakistan – are bust due to huge indebtedness to China as a result of unaffordable, ambitious infrastructure projects. These loans were granted without concern about credit ratings or the ability to repay, and accused of being politically-motivated “debt traps”. But these have become China’s “debt traps” and now protests and pushbacks take place in these countries against Beijing. Now China must forgive loans, restructure them, or walk away and let more Sri Lankan-style collapses occur.

Clearly, China’s show of force after Nancy Pelosi’s Taiwan visit, and its military aggressions, distract from this ongoing made-in-China economic train wreck. In November, China’s top Communist Party leaders will gather in Beijing for a critical meeting ahead of next year’s national congress. The theme will be to focus on “the major achievements and historical experience of the party’s struggle in the past century” and to address “why we have succeeded in the past and how we can continue to succeed in the future”.

China’s immediate past has been truly impressive, and lifted the country out of abject poverty. But given Xi’s economic mismanagement, combined with his loyalty to Putin who is the sworn enemy of all his Western customers, China’s future looks not only dim but potentially disastrous.

TO BE CLEAR. Love your comments and I have some of the smartest readers around, but if you libel anyone (smear without evidence) or personally insult anyone else who's commenting I will remove your comment. Cheers.

Unbelievable. Thank you for the clear and understanding of this world shattering paradigm.

Now if we only had a leader of this country, truly understand what next steps Canada should take outside of a photo opp.

Bruce